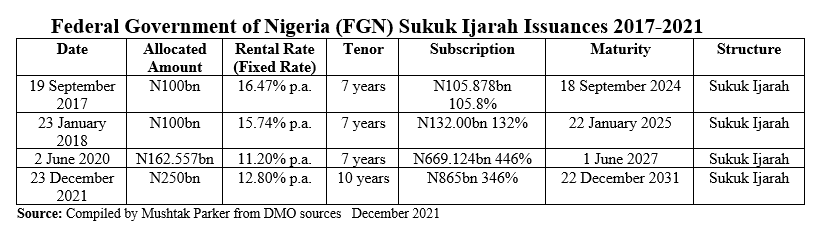

The Federal Government of Nigeria (FGN) continued to build up a yield curve for its naira-denominated FGN Sovereign Domestic Sukuk with its fourth offering to date on 23 December 2021 – a benchmark N250 billion (US$610 million) Sukuk Forward Ijarah linked to road infrastructure development.

Perhaps it is not surprising that the latest transaction issued by the Debt Management Office (DMO) of the Nigerian Ministry of Finance attracted an “unprecedented subscription level of over N865 billion (US$2.09 billion),” which means the issuance was oversubscribed by 346%.

The DMO’s Sukuk issuance strategy is unique in that it is entirely focused on financing the rehabilitation and reconstruction of key road projects across the six geopolitical zones and the Federal Capital Territory. This strategy for various reasons could be evolved as a model for other countries – both in developed and developing economies.

According to the G20 and World Bank, Sukuk are particularly suited to fund infrastructure projects, although in recent years banks and corporates have resorted to Sukuk to boost Tier I and II capital under Basle requirements, refinancing existing more expensive conventional debt and for balance sheet purposes.

The disappointing aspect of Nigeria’s first mover advantage in infrastructure-linked Sukuk is that it has failed to spur a market for quasi-sovereign, corporate and social issuances.

According to Nigerian banking sources, Dangote Cement, a major player in the country’s road infrastructure reconstruction programme in its capacity as the country’s major cement producer, was contemplating a debut Sukuk just prior to the onset of the coronavirus pandemic. But market conditions most likely put paid to that ambition, albeit the potential is good depending on the reputation and financial stability of the issuer. There are also reports of more state governments following Osun State in issuing Sukuk.

An important development is the opening up of investment in FGN Sukuk by the 22 or so pension providers regulated by the National Pension Commission (PenCom) subject to its eligibility criteria. In fact, Patience Oniha, Director-General of the DMO, met with senior PenCom officials on 1 December 2021 and discussed inter alia “recent developments in the sector and the plans for the two institutions to cooperate in areas of mutual interest.”

The FGN Sukuk embodies two key sustainability features – infrastructure and financial inclusion. “We consider Sukuk to be one of the useful and accepted products for raising funds,” explains Oniha. “The proceeds from the issuance will be used solely for the construction and rehabilitation of 44 arterial roads across the six geopolitical zones of the country. Issuing further Sukuk in 2022, will depend on eligible projects in the 2022 Appropriation Act.”

The Sukuk certificates, which are guaranteed by the government, are available to both institutional and retail investors. Demand for FGN securities in the domestic market, stresses Oniha, is strong. The minimum subscription for retail investors for the latest N250bn offering is only ₦10,000 (US$24.38). DMO analysis reveals high levels of subscription from banks and fund managers (including pension funds), as well as non-interest (Islamic) financial institutions, ethical funds, cooperative societies and retail investors.

The journey of retail investors is revealing – 5% for the debut issuance in 2017, followed by 17.33% for the second issuance in 2018, to over 18% for the third issuance in 2020. The retail subscription share for the 2021 issuance has yet to be released.

The increasing level of participation by a more diverse and larger number of investors, stressed the DMO, “is a confirmation that the DMO’s objectives of issuing sovereign Sukuk to grow the domestic investor base and promote financial inclusion is being achieved. In addition, the high subscription level is proof of investors’ acknowledgement of the impact the first three Sukuk issuances totalling N362.577 billion (US$880 million) issued between 2017 and 2020 has had on the development of road infrastructure in Nigeria.”

The Nigerian DMO is headed by the experienced and respected Patience Oniha, ex-CEO of Standard Chartered Bank (Nigeria) and senior MoF official for many years. Her international reputation belies her soubriquet as Nigeria’s ‘Bond Lady’ having proactively steered the FGN bond issuance programme for almost a decade. Since 2017 she has also directed the DMO’s Sukuk issuance strategy and programme. According to Oniha, sovereign Sukuk diversifies the product range available to investors in the domestic financial market, widens the investor base and promotes financial inclusion by attracting several first-time retail investors.

Oniha in fact closed Nigeria’s fourth sovereign domestic Sukuk issuance – a 10-year ₦250bn (US$610m) Ijarah (Leasing) offering maturing in 2031 on 23 December 2021. This brings Nigeria’s aggregate naira-denominated Sukuk issuance to ₦612.57 billion (US$1.49 billion).

The Sukuk was issued on 16 December 2021 through FGN Roads Sukuk Company 1 PLC on behalf of the obligor, the Federal Government of Nigeria, and is priced at a fixed rental rate of 12.8% per annum. The transaction involved several Nigerian financial institutions as receiving banks and placement agents, including the country’s two dedicated non-interest (Islamic) banks Taj Bank and Jaiz Bank, as well as local subsidiaries of the UK’s Standard Chartered Bank and South Africa’s Standard Bank, namely Stanbic IBTC Bank.

The DMO had mandated Greenwich Merchant Bank, Stanbic IBTC Capital and Vetiva Capital Management to act as Issuing Houses to the transaction. Stanbic IBTC Bank, Zenith Bank, Lotus Bank, Sterling Bank were joined by Jaiz Bank and Taj Bank as Receiving Banks.

According to the DMO, FGN Sukuk IV has several sustainability and ethical attributes. These include responsible investing (the proceeds are dedicated to tangible road infrastructure projects; financial inclusion for non-interest investors with the aim also of further developing the savings culture in Nigeria; ethical investment for investors who are ethically minded; low risk as the certificates are guaranteed by the FGN; liquidity since the certificates can be traded on the two top local stock exchanges and qualify as liquid assets for banks and other institutions; and the Sukuk certificates may be used as collateral for securing credit facilities from financial institutions.

The Sukuk certificates are listed on the FMDQ Securities Exchange, Nigeria’s largest bourse, and the Nigerian Exchange Limited. With the listing, Sukuk certificate holders can trade them while new investors have an opportunity to buy the certificates in the secondary market, thus unlocking vital liquidity in the capital market.

The development impact of Sukuk is clearly visible – improved road infrastructure within and outside Nigerian cities, timely completion of designated projects and the multiplier effects associated with construction of capital projects such as roads. This, says the DMO, “has brought reprieve to road users, improved travel times between major commercial cities, linked borrowing and government expenditure to specific critical projects, helped increase the flow of cargo and passenger traffic across major cities, and improved infrastructure delivery across the country.

“The impact of the sovereign Sukuk on road infrastructure in terms of job creation, travel time, safety and movement of goods have made the Sukuk a beneficial financial instrument for financing economic growth and development.”