UAE Government Domestic Treasury Sukuk Auctions Raise AED5bn (US$1.4bn) in First Quarter 2024 Driven by Market Buoyancy and Robust Demand and Contributing to Building an AED Yield Curve

The dirham-denominated Islamic Treasury Sukuk (T-Sukuk) first introduced by the UAE Ministry of Finance (MoF) in collaboration with the Central Bank of the UAE (CBUAE) on 15th May 2023 is gaining traction as sovereign domestic Sukuk issuances to regulate liquidity management and reserve requirements of Islamic financial institutions at the central banks gains momentum beyond traditional markets where Islamic finance is deemed of systemic importance in the banking system.

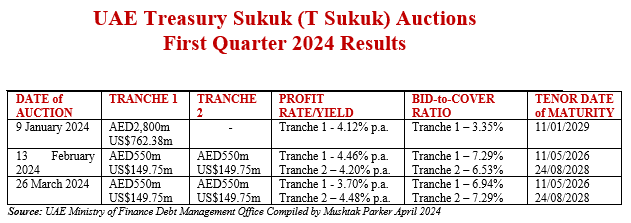

In FY 2023 the aggregate volume of T Sukuk issued by the MoF/(CBUAE) in 10 auctions held during the year amounted to AED5,000 mn (US$1,361.40 mn) through auctions held in May, June, August, October, and November.

In the first quarter of 2024 alone, the aggregate volume of T Sukuk issued by the MoF/(CBUAE) had already equaled the AED5,000 mn issued in the whole of 2023 according to the latest data from the UAE Treasury. The latest auction of T Sukuk was held on 28 March 2024 which raised AED1.1 bn (US$299.51 mn) in two tranches of AED550 mn (US$149.75 mn) each.

The AED550 mn Tranche 1 which matures on 11 May 2026 was priced at a fixed profit rate of 3.70% p.a. payable semi-annually in arrears, with a Bid-to-Cover Ratio of 6.94%. The AED550 mn Tranche 2 which matures on 24 August 2028 was priced at a fixed profit rate of 4.48% p.a. payable semi-annually, with a Bid-to-Cover Ratio of 7.29%.

“The auction,” according to the UAE Treasury Ministry, “witnessed a strong demand through the eight primary dealers for the 3-year and 5-year tranches of the Islamic T-Sukuk, with bids received worth AED7.83 bn (US$2.13 bn) and an oversubscription by 7.1 times. The success is reflected in the attractive market driven prices, which was achieved by a spread of 4 basis points over the US Treasuries with similar maturities. The Islamic T-Sukuk issuance programme will contribute to building the UAE dirham denominated yield curve, providing safe investment alternatives for investors, strengthening the local debt capital market, developing the investment environment, as well as supporting sustainable economic growth.”

The UAE MoF and CBUAE announced the launching of the T-Sukuk in April 2023. According to UAE Minister of State for Financial Affairs, Mohamed Bin Hadi Al Hussaini, the introduction of the T Sukuk “reaffirmed the UAE’s keenness to strengthen the Islamic economy and build a pioneering investment infrastructure to boost it as one of the key pillars of the national economy. The T-Sukuk are Sharia’a-compliant financial certificates, and they will be traded to reflect the local return on investment, support economic diversification and financial inclusion, as well as contribute to achieving comprehensive and sustainable economic and social development goals.”

All the T Sukuk offerings are issued under the unlimited UAE Treasury Sukuk Programme. The Sukuk were issued by the UAE Federal Government Sukuk Programme Ltd acting as Trustee and Lessor on behalf of the Seller, Obligor, Lessee and Servicing Agent, namely The Government of the United Arab Emirates, acting through the Ministry of Finance of the United Arab Emirates.

Building a Yield Curve

The T-Sukuk issuance programme, added Minister Al Hussaini, will contribute to building the UAE dirham denominated yield curve, providing safe investment alternatives for investors, strengthening the local debt capital market, developing the investment environment, as well as supporting sustainable economic growth.

The Sukuk structure is based on Murabaha/Ijara assets with the asset pool comprising 54% Ijara assets and 46% Murabaha receivables.

The Sukuk, was issued via eight primary dealers, with the UAE Central Bank acting as the issuing and payment agent. To facilitate the smooth implementation of the T-Sukuk initiative, the MoF published a robust Primary Dealers code and onboarded eight banks namely Abu Dhabi Islamic Bank, Dubai Islamic Bank, Abu Dhabi Commercial Bank, Emirates NBD, First Abu Dhabi Bank, HSBC, Mashreq and Standard Chartered as Primary Dealers to participate in the T-Sukuk primary market auction and to actively develop the secondary market.

The T Sukuk certificates are listed on the Official List of the Dubai Financial Services Authority and on Nasdaq Dubai.

The launching of the T-Sukuk, he added, incorporates a series of issuances, to attract a new category of investors and support the sustainability of economic growth. The issuance of T-Sukuk, thus is also aimed at enhancing the UAE’s economic competitiveness by providing high-quality Islamic assets at competitive prices. This will support the CBUAE in managing liquidity within the banking sector and boosts the size of financial investments, which will reflect positively on the country’s economy, investment environment, per capita income, and gross national income.

In addition, issuing the T-Sukuk in local currency would contribute to building a local currency bond/Sukuk market, diversifying financing resources, boosting the local financial and banking sector, providing safe investment alternatives for local and foreign investors, as well as helping build a UAE Dirham-denominated yield curve, thereby strengthening the local financial market and developing the investment environment.

Until recently, with Malaysia being a notable exception, there has been a disconnect between the Islamic banking policies and aspirations of IsDB member states with market practice at the regulatory and supervisory levels especially in managing the short-term liquidity requirements of Islamic banks and Islamic Banking Windows (IBWs) at conventional banks, and the management of the capital and other statutory reserves of authorised financial institutions in their respective jurisdictions.

Malaysia has led from the front with Malaysian Government Securities, sovereign domestic Sukuk and a range of other Sharia’a compliant Treasury instruments going back to the 1980s, steered by a proactive government and a forward-looking Bank Negara Malaysia (the central bank) especially under Governor Dr Zeti Akhtar Aziz.

In recent years, Bahrain, Indonesia, Brunei, Saudi Arabia, Pakistan, Turkiye, Kuwait, Qatar to varying degrees have become regular issuers of domestic sovereign Sukuk precisely for the short-term liquidity management needs of Islamic banks and IBWs in their jurisdictions and the parking of their statutory capital and reserve requirements.

In these markets where Islamic banking is of systemic importance, the development of the local regulatory liquidity management architecture based on domestic Sukuk instruments, has been a major boost, albeit has taken a few decades to get there. The fact that the UAE has now joined this core cohort of countries with regular issuance of Sharia’a compliant sovereign domestic liquidity and investment management instruments is important to institutionalise this vital practice and service for the orderly and effective development of the Islamic finance market and its depth.

The issuance of Islamic treasury Sukuk comes within the framework of the UAE’s commitment to developing capital market activities and consolidating its position as a global financial hub.

“This issuance,” added the Ministry of Finance, “reaffirms the strength and stability of the financial system and the confidence of local and international investors in the UAE’s ability to develop the financial sector in accordance with monetary policies and strategic plans. With the development of an effective infrastructure for the financial markets, we are confident that this issuance will contribute to supporting the market for Sukuk denominated in the local currency and issued by the public sector in the country.

“It will also enhance the competitiveness of the local financial markets and enable market participants in the UAE to maintain a single, transparent, diversified and sustainable liquidity pool in Dirhams. Furthermore, it will contribute to the implementation of the new Dirham Monetary Framework (DMF) and support the ongoing work to establish the Dirham risk-free pricing benchmark (yield curve), which would stimulate more domestic market activities to support the sustainability of the country’s economic growth.”

The T-Sukuk, according to the MoF, will be issued initially in 2/3/5-year tenures, followed by a 10-year Sukuk later. The structuring of Islamic Sukuk has been approved by the Higher Sharia’a Authority at the CBUAE, which cooperates with the relevant authorities to standardise and unify the practices of Islamic financial institutions to be compatible with internationally recognised Sharia’a standards and best practices.

The T-Sukuk programme, says the MoF, was developed in uniform pricing (the Dutch Auction) for final bid acceptance of bids and final allocation amounts, regardless of the lower-priced bids received, to ensure full transparency in accordance with global best practices for Sukuk structuring.

These Sukuk will provide safe investment alternatives for investors which contributes to developing the UAE’s investment environment.